How to Boost Your Credit Score by 200 Points in 30 Days

Achieving an increase, in your credit score within a month might appear challenging but its definitely possible. While its not very common to witness such a jump with efforts and effective strategies you can make substantial improvements. Lets delve into the realm of credit scores and explore steps you can take to give your score a boost.

A Brief Overview of the Evolution of Credit Scores

The practice of evaluating creditworthiness has been in existence for centuries. The modern credit scoring system that we are familiar with today originated during the mid 20th century. Here’s a concise summary outlining the roots of credit scores;

Pre 20th Century;

Prior to the advent of credit scores lending decisions were primarily based on relationships. Merchants and lenders maintained records of individuals who owed them money and lending choices were often influenced by familiarity, trustworthiness and reputation. While there were some ledgers and blacklists available there was no method for assessing an individuals creditworthiness across merchants or regions.

1950s. The Birth of Credit Scores;

The foundation of our credit scoring system can be traced back, to the 1950s when engineer William R. Fair and mathematician Earl J. Isaac established Fair, Isaac and Company (now known as FICO).They introduced a method to evaluate the creditworthiness of consumers by utilizing techniques that assess their ability to repay loans.

In the 1970s there was a change, in regulations with the passing of the Equal Credit Opportunity Act in 1974. This act made it illegal for lenders to consider factors such as race, gender and nationality when assessing creditworthiness. Consequently there arose a need for a systematic approach to assess creditworthiness, which led to the development of the credit score.

During the 1980s and 1990s FICOs credit scoring model gained success. Became widely adopted by lenders. In fact major credit bureaus started using variations of the FICO model during this period. Moreover with more companies entering the market and an increase in credit card usage during the 1990s we witnessed diversification in credit scoring models.

Get Credit Repair

Moving into the 2000s consumers were granted access to their credit scores through The Fair and Accurate Credit Transactions Act of 2003. This act gave every citizen the right to receive a copy of their credit report from each credit bureau – Equifax, Experian and TransUnion. This increased transparency empowered individuals to have an understanding of their well being and make decisions about their credit.

In todays world credit scores play a role in financial matters such, as obtaining mortgages or qualifying for specific job opportunities.

Advancements, in technology and the utilization of data analytics have enhanced credit scoring models. Companies such as Credit Karma and others now provide credit scores and credit monitoring services to millions of individuals.

Get Credit Repair

While FICO continues to be a player in the industry there are now models in use. One such model is VantageScore, which was introduced in 2006 through a collaboration among the three credit bureaus. Its objective was to establish a methodology for calculating credit scores.

In essence the history of credit scoring reflects changes, technological advancements and developments within the industry. These transformations have shaped the evolution of the system moving from trust based lending to models. However its fundamental purpose remains unchanged; to provide an assessment of an individuals creditworthiness.

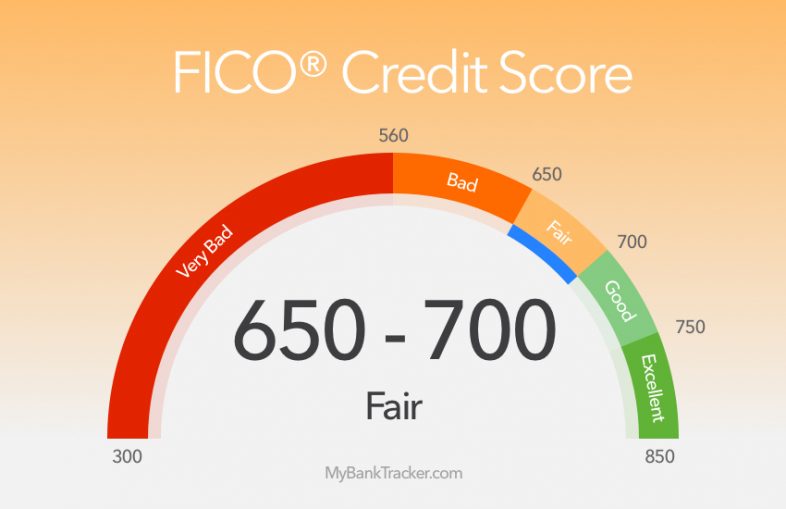

Understanding Credit Scores;

Credit scores are summaries that evaluate your creditworthiness based on your credit history. Several factors influence this score;

1. Payment History (35%); This factor takes into account your record of bill payments, including any instances of missed payments.

2. Amounts Owed (30%); It considers both the total amount of debt you have and your utilization rate.

3. Length of Credit History (15%); The age of your credit accounts and their average age across all accounts play a role, in this factor.

Here are some steps you can follow to enhance your credit score;

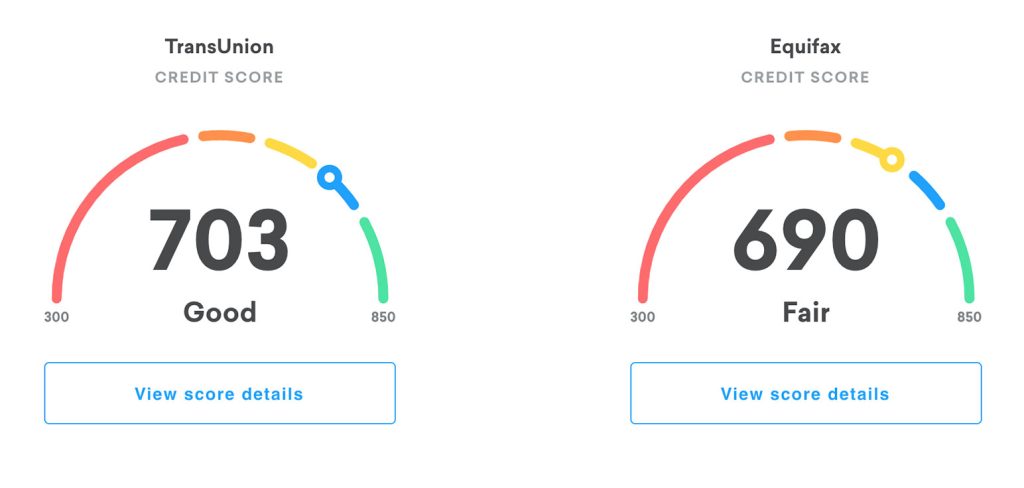

1. Make sure to review your credit report and check for any errors. Obtain a copy of your credit report, from Equifax, Experian and TransUnion (the credit bureaus). Examine the report thoroughly to identify any inaccuracies, such as payments or unauthorized accounts. If you come across any mistakes file a dispute with the credit bureau. Correcting these errors can potentially boost your credit score.

2. Work on reducing the balances on your credit cards. Your credit utilization rate, which compares the balance on your card to its limit affects your score. Aim to maintain a utilization ratio below 30%. Paying off balances promptly can lead to improvements in your score.

3. Engage in communication, with your creditors if you have records of payments. Consider reaching out to them and requesting a “goodwill adjustment” that removes the payment from being reported on your account. For charged off accounts try negotiating a “pay for delete” arrangement where the creditor agrees to remove the mark from your report once payment is received.

By implementing these strategies over time you can work towards improving and elevating your credit score.

Here are some strategies you can use to enhance your credit score;

1. Consider being added as an user, on someone Credit card with a good payment history and low credit utilization. This can positively impact your score by reflecting their credit behavior on your report.

2. It’s advisable to avoid applications for credit as each application leads to an inquiry that can slightly lower your score. Refrain from seeking credit to prevent these minor dips.

3. If you currently have one type of credit account it may be beneficial to diversify your credit mix. However ensure that you can responsibly manage any accounts before opening them.

Get Credit Repair

4. Timely bill payment is crucial for maintaining a score. Consider setting up reminders or automating payments to ensure that they are made on time.

5. You may want to request increases in the credit limits of your existing cards without triggering an inquiry into your credit history. Having a limit can help lower your utilization rate.

6. If you ever feel overwhelmed by the complexities of managing your finances it could be helpful to seek assistance from professionals such as credit counselors or reputable credit repair companies. They can provide strategies. Even negotiate on your behalf.

Remember to stay informed, about the guidelines and any updates or changes related to credit scores and their evaluation criteria. Having knowledge in this area will empower you when making decisions.

Now lets discuss some things you should avoid;

1.

Closing old credit cards can have an impact, on your credit scores because it reduces the length of your credit history and increases your credit utilization. Additionally opening accounts can be detrimental as it lowers the age of your accounts and results in multiple hard inquiries on your credit report. It is crucial not to neglect debts because collections or unpaid debts can significantly damage your credit scores.

While following the strategies mentioned above can lead to improvements in your credit score it’s important to understand that achieving a 200 point increase within 30 days is quite exceptional. Several factors such as your credit score details in your credit report and financial habits all play a role in determining how quickly you can improve. For some individuals reaching such a goal may take longer.

Get Credit Repair

Consistency is key throughout this journey. Continuously monitor your credit report maintain habits and over time you will see a transformation in how lenders perceive your creditworthiness. Remember that patience and persistence are just as crucial, as having a strategy when aiming for a credit score.